In the modern business landscape, the solo entrepreneur has become a driving force, characterized by innovation, agility, and a strong desire for independence. Individuals are increasingly choosing to launch their own ventures, moving away from traditional employment structures. This surge in independent entrepreneurship has brought various legal business structures into prominence, each presenting distinct advantages and potential drawbacks.

Among these, the Limited Liability Company, particularly its variation designed for individual ownership, known as the Single-Member LLC, has garnered substantial popularity and widespread adoption.We will delve into its significant legal, financial, and administrative implications, offering a detailed and comprehensive guide for anyone considering this highly favored business structure.

Defining the Single-Member LLC: A Hybrid Business Structure

At its fundamental core, a Single-Member LLC functions as a unique business entity that skillfully combines the robust liability protection typically associated with a corporation with the operational simplicity and the streamlined pass-through taxation characteristic of a sole proprietorship. As its name explicitly indicates, this entity is exclusively owned by a single individual, who is commonly referred to simply as the “member” of the LLC.

The Concept of Limited Liability

The most compelling and attractive characteristic of any Limited Liability Company, including a Single-Member LLC, is the principle of “limited liability.” This crucial legal concept signifies that the personal assets of the owner are legally and unequivocally separated from the debts and liabilities incurred by the business itself.

Should the business ever encounter legal challenges, financial distress, or even face bankruptcy proceedings, the owner’s personal possessions such as their family home, personal vehicle, and individual savings accounts are generally safeguarded from the claims of creditors. This separation represents a pivotal difference when contrasted with a sole proprietorship, wherein the owner’s personal and business liabilities are inextricably linked and indistinguishable in the eyes of the law.

The “Company” Designation

Despite being owned by a single individual, a Single-Member LLC is formally recognized as a distinct and separate legal entity by the state in which it is formed. This important legal distinction grants a level of professionalism and credibility that a mere sole proprietorship often lacks. It empowers the business to independently enter into legally binding contracts, establish dedicated business bank accounts, and acquire and hold assets in its own name, completely separate from the individual owner’s personal identity and finances.

Pass-Through Taxation: The Inherent Default Status

One of the defining and most beneficial attributes of a Single-Member LLC, by default, is its pass-through taxation status. This essential feature means that the LLC itself is not subject to federal income tax at the entity level. Instead, the profits and any losses generated by the business are directly “passed through” to the owner’s personal income tax return.

The owner is then responsible for reporting these business activities on their personal tax form, often using Schedule C of Form Ten-Forty, mirroring the reporting method for a sole proprietorship. This ingenious tax structure effectively circumvents the issue of “double taxation,” a scenario commonly associated with C-corporations, where both the corporation and its individual shareholders are taxed on the same profits.

The Journey of Formation and Registration: Steps to Establishing Your Single-Member LLC

Establishing a Single-Member LLC involves a series of specific and legally mandated steps. While the precise procedural requirements may exhibit slight variations from one state to another, they generally adhere to a widely recognized and consistent pattern. Diligent adherence to these procedural guidelines is absolutely critical for achieving official legal recognition of the entity and, more importantly, for effectively maintaining the integrity of the liability shield it is designed to provide.

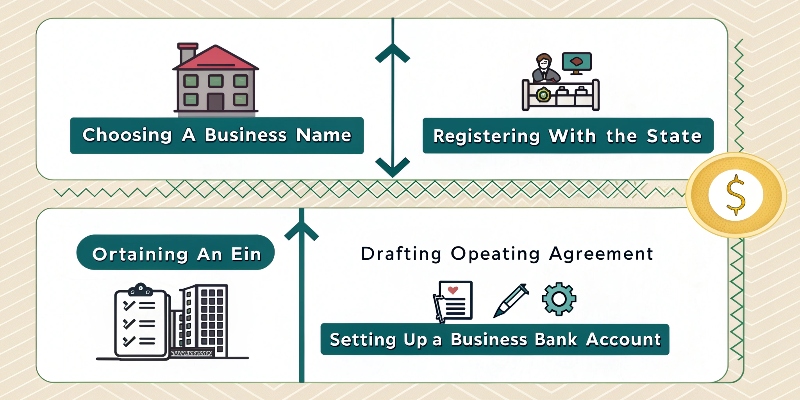

The Process of Choosing a Business Name

The foundational step in forming an LLC is to meticulously select a business name that is both distinctive and available for use. State regulations typically mandate that the chosen name must incorporate an LLC designator, such as “LLC,” “L.L.C.,” or the full phrase “Limited Liability Company.” It is strongly recommended to conduct a comprehensive name availability search with the respective Secretary of State’s office or equivalent state agency to preempt any potential conflicts with existing business names.

Designating a Registered Agent

Every Limited Liability Company is legally obligated to appoint a “registered agent.” This can be either a specific individual or a professional service provider who bears the responsibility of receiving all official legal and governmental documents on behalf of the LLC. The designated registered agent must possess a verifiable physical street address a Post Office Box is generally not acceptable within the state where the LLC is formally established, and they must be reliably available during standard business hours to accept these critical correspondences.

The Act of Filing Articles of Organization

This document stands as the quintessential and foundational legal instrument for the formation of an LLC. Upon submission to the Secretary of State or the relevant state agency, the Articles of Organization typically include vital information such as the LLC’s chosen legal name, the name and physical address of its designated registered agent, and in some jurisdictions, a brief statement outlining the general purpose or nature of the business. The successful filing of this document formally and legally brings the entity into existence.

Crafting an Operating Agreement: The Governing Document

Although frequently overlooked by solo entrepreneurs due to the single-owner nature of the entity, an Operating Agreement is an exceptionally vital internal legal document for a Single-Member LLC. While it may not always be a legally mandated requirement in every state, its creation is profoundly recommended as it explicitly outlines the operational and financial understandings of the LLC.

Securing an Employer Identification Number (EIN)

Even though a Single-Member LLC without employees is generally considered a disregarded entity for federal income tax purposes by the Internal Revenue Service, it typically still requires an Employer Identification Number, often referred to as an EIN.

Adhering to State and Local Regulatory Compliance

Beyond the primary state-level registration, Single-Member LLCs must also diligently comply with a myriad of additional state and local regulatory stipulations. This often includes the imperative of obtaining any necessary business licenses and specific operational permits. The precise nature and scope of these requirements can exhibit considerable variation depending on the particular industry in which the business operates and its specific geographical location.

Understanding the Taxation of a Single-Member LLC: Exploring Your Options

One of the most compelling and appealing attributes of a Single-Member LLC is the inherent flexibility it offers in its tax treatment. While it is generally taxed by default in a manner akin to a sole proprietorship, owners possess the significant advantage of being able to elect different methods of tax treatment based on their specific financial circumstances and business objectives.

Default Taxation: The Disregarded Entity Status

For the purposes of federal income taxation, a Single-Member LLC is automatically classified as a “disregarded entity.” This classification implies that the Internal Revenue Service does not perceive the LLC as a separate taxable entity distinct from its owner. Consequently, all income generated and all expenses incurred by the business are reported directly on the owner’s personal income tax return, typically using Form Ten-Forty, Schedule C.

The Option to Elect Corporate Taxation

While the default tax classification for an SMLLC is that of a sole proprietorship, a Single-Member LLC owner possesses the strategic option to elect for the LLC to be taxed as a corporation. This election can take one of two primary forms: an S-corporation or a C-corporation.

The S-Corporation Election

Electing S-corporation status can present substantial tax advantages for certain Single-Member LLC owners. Under an S-corp election, the owner has the ability to draw a “reasonable salary” as an employee of their own LLC. This designated salary is subject to FICA taxes, which include both Social Security and Medicare contributions.

The C-Corporation Election

While considerably less common for Single-Member LLCs, an owner does retain the option to elect for the LLC to be taxed as a C-corporation. Under this classification, the business entity would be subject to corporate income tax at the corporate level. Any subsequent profits that are distributed to the owner in the form of dividends would then be taxed once more at the individual level, leading to the phenomenon known as “double taxation.”

State-Specific Tax Implications

It is critically important for owners to recognize that state tax regulations can often diverge significantly from federal tax rules. Some states may impose their own distinct franchise taxes or require the payment of annual fees specifically on LLCs, irrespective of their chosen federal tax classification. Therefore, Single-Member LLC owners must diligently research and understand the specific tax requirements and obligations mandated by their respective states.

Maintaining Your Single-Member LLC: Preserving the Liability Shield

The invaluable protection of limited liability afforded by a Single-Member LLC is neither an inherent right nor an automatic guarantee. It is a privilege that must be actively and diligently preserved through the consistent adherence to sound legal and financial best practices. Failure to uphold these standards can lead to a court disregarding the LLC’s separate identity, thereby exposing the owner to personal liability.

The Absolute Necessity of Separating Personal and Business Finances

This practice stands as arguably the most critical and foundational aspect of effectively maintaining the liability shield. The owner must rigorously and unequivocally separate all personal and business financial accounts, including bank accounts, credit cards, and all corresponding financial records. The act of “commingling” funds, where personal and business monies are intermixed, can provide a legal basis for a court to “pierce the corporate veil,” which would result in the owner being held personally liable for the debts and obligations of the business.

The Importance of Meticulous Record Keeping

Maintaining accurate, comprehensive, and organized business records, encompassing financial statements, all business contracts, and even informal meeting minutes for an SMLLC, serves as undeniable evidence that the business is being operated as a distinct and separate legal entity. Such diligence strengthens the defense against any claims that the LLC is merely an alter ego of the owner.

Strict Adherence to Operating Agreement Provisions

Even though an Operating Agreement is an internal document, consistently following the guidelines, rules, and procedures explicitly laid out within it reinforces the legal legitimacy of the LLC as a genuinely distinct and independent entity. This demonstrates a commitment to formal business governance.

Timely Annual Filings and Fee Payments

Ensuring the prompt and timely payment of all annual report fees, any applicable franchise taxes, and all other state-mandated periodic filings is absolutely essential for keeping the LLC in good standing with the state regulatory authorities. Any failure to comply with these ongoing requirements can unfortunately result in the administrative dissolution of the LLC or, critically, the loss of its vital limited liability protection.

Scenarios Where a Single-Member LLC Excels

The Single-Member LLC is particularly well-suited and highly advantageous for a diverse array of solo entrepreneurial endeavors and small business operations across various sectors.

Independent Freelancers and Professional Consultants

Individuals who offer specialized professional services, such as highly skilled graphic designers, accomplished freelance writers, insightful marketing consultants, and adept IT specialists, derive immense benefit from the protective shield of limited liability and the simplified tax structure provided by an SMLLC.

Online E-commerce Ventures

Entrepreneurs engaged in online retail and e-commerce operations can strategically leverage the Single-Member LLC structure to safeguard their personal assets from potential product liability claims, unforeseen contractual disputes, or other business-related legal challenges that may arise from their online sales activities.

Small-Scale Service-Based Businesses

Sole proprietors who operate various small-scale service-based businesses, such including dedicated landscaping services, professional cleaning companies, or personalized fitness training, can significantly professionalize their operations and acquire invaluable liability protection by adopting the SMLLC structure.

Strategic Real Estate Investment Holdings

Single-Member LLCs are frequently and strategically employed by real estate investors to hold individual rental properties. This specific application offers crucial asset protection for each property, safeguarding the owner from potential tenant lawsuits, property-related liabilities, or other unforeseen claims associated with their real estate portfolio.

Nascent Side Hustles and Passion Projects

For individuals who are initiating a side business or pursuing a passion project that possesses inherent potential for growth or carries any degree of liability risk, a Single-Member LLC offers a relatively low-cost and administratively straightforward pathway to establish essential personal asset protection right from the very beginning of their entrepreneurial journey.

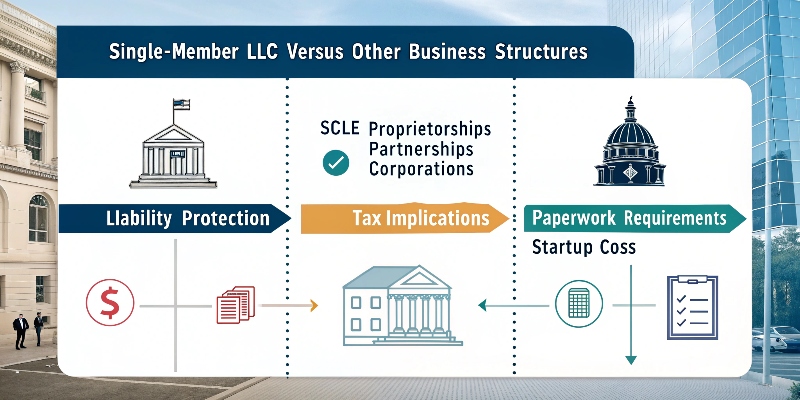

Single-Member LLC Versus Other Business Structures: A Comparative Analysis

Grasping the precise positioning of the Single-Member LLC within the broader array of available business structures is absolutely fundamental for solo entrepreneurs to make a thoroughly informed and strategically sound decision regarding their entity choice.

Single-Member LLC Compared to a Partnership

A partnership, by its very definition, involves two or more owners who collectively share in the profits and losses of a business. A Multi-Member LLC operates on principles similar to a Single-Member LLC but necessitates a considerably more comprehensive and detailed operating agreement. This expanded agreement is vital for clearly defining the specific roles, responsibilities, profit and loss distribution methodologies, and robust dispute resolution mechanisms among all the multiple members to ensure harmonious and effective collaboration.

Single-Member LLC Compared to a Corporation

Corporations, particularly C-corporations, are inherently more complex and demanding to form and maintain. They are subject to more stringent compliance requirements, involve more elaborate administrative burdens, and often feature more formal and rigid governance structures. C-corporations, for example, are also uniquely susceptible to the issue of double taxation.

Conclusion: The Empowering Choice for the Modern Solo Entrepreneur

The Single-Member LLC stands as a remarkably powerful and inherently flexible business structure, offering a unique blend of personal asset protection, operational simplicity, and significant tax advantages. For the contemporary solo entrepreneur navigating the dynamic and often unpredictable world of independent business, the SMLLC provides a robust foundation for building a successful venture while safeguarding personal assets.